Understand the new NPS exit and withdrawal rules 2025, higher lump sum limits, lower annuity rules, and what these changes mean for your retirement planning.

Recently, PFRDA introduced new NPS (National Pension System) Exit and Withdrawal rules. These changes in many ways, are game changers. Let us discuss these changes in detail in this post.

New NPS Exit and Withdrawal Rules 2025: What Changed and Why

The PFRDA (Exits and Withdrawals under the National Pension System) (Amendment) Regulations, 2025, represent a significant shift in how pension wealth is managed and accessed in India. By replacing the 2015 framework, these amendments modernise terminology, extend the participation period, and introduce more flexible payout options such as systematic withdrawals.

1. Change in Terminology and Structure

The regulations replace the term “Permanent Retirement Account” with “Individual Pension Account” and replace the word “corpus” with “wealth”. This is not cosmetic. It reflects that each account is treated independently.

If a subscriber has multiple accounts — for example, a government account and an All Citizen account — each account is now governed independently for exit, withdrawal, and annuity purposes. This gives subscribers better control and clarity over each stream of retirement savings.

The term “deferment” is also formally defined, meaning the subscriber may postpone lump sum withdrawal or annuity purchase.

2. Subscriber Categorisation

Subscribers are now formally categorised as Government Sector, Non-Government Sector, and NPS-Lite/Swavalamban. Each category has its own exit and withdrawal framework.

This clarity reduces confusion and ensures that rules are applied correctly based on the type of subscriber rather than treating all subscribers identically.

3. Ability to Stay Invested Until Age 85

Both government and non-government subscribers can now remain in NPS until age 85. They may defer both lump sum withdrawal and annuity purchase.

While this provides flexibility for financially independent retirees, for most investors this extension is of limited practical value because retirement expenses generally start much earlier than 85.

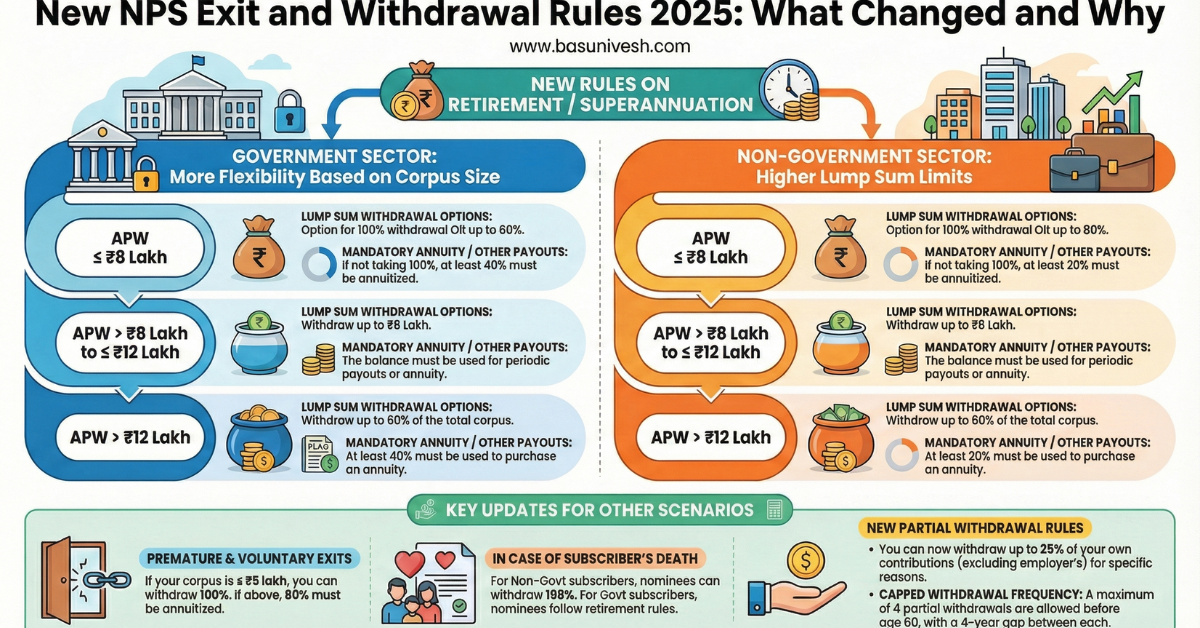

4. Exit Rules for Government Subscribers

At retirement, at least 40% of the wealth must be used to buy an annuity. The balance can be withdrawn as lump sum or through systematic withdrawals.

If the wealth is Rs.8 lakh or less, the subscriber can withdraw 100% without any annuity.

If the wealth is between Rs.8 lakh and Rs.12 lakh, up to Rs.6 lakh can be withdrawn and the balance must be used for annuity or systematic withdrawals over at least six years.

If a government employee resigns or is removed, the exit is treated as premature, and normally 80% must be used for annuity unless the wealth is Rs.5 lakh or less.

5. Exit Rules for Non-Government Subscribers

Non-government subscribers normally exit upon reaching the age of 60. The 15-year condition refers to minimum eligibility for certain withdrawal benefits but does not convert exits before 60 into normal exits.

However, exits before age 60 are treated as premature exits and have stricter conditions.

At normal exit (age 60):

At least 20% must be used for annuity and up to 80% can be withdrawn.

If the wealth is Rs.8 lakh or less, 100% can be withdrawn.

If the wealth is between Rs.8 lakh and Rs.12 lakh, up to Rs.6 lakh can be withdrawn and the rest must be annuitised or withdrawn gradually over six years.

For late joiners (joining at age 60 or later), if the wealth is Rs.12 lakh or less, the entire amount can be withdrawn.

This flexibility is beneficial, but it does not remove the core issue — annuities remain low-return and poor inflation protectors.

6. Physical Incapacity

If a subscriber is permanently incapacitated and medically certified as unfit to continue employment, the exit is treated as a normal retirement exit rather than premature exit.

This protects subscribers who are forced into early retirement due to health reasons.

7. NPS-Lite and Swavalamban Subscribers

For these subscribers, the threshold for full lump sum withdrawal has been increased to Rs.2 lakh.

This is a meaningful improvement for low-income subscribers for whom annuities were impractical.

8. Special Exit Scenarios

If a subscriber renounces Indian citizenship, the entire wealth can be withdrawn.

If a subscriber is missing, 20% of the wealth can be released as interim relief after filing an FIR and indemnity bond. The remaining amount is released only after court declaration.

9. Partial Withdrawals and Loan Collateral

Subscribers can withdraw up to 25% of their own contributions for specific purposes such as medical needs or housing.

They can also use their NPS account as collateral for loans by allowing financial institutions to place a lien on the account.

This improves flexibility but also increases the risk of eroding retirement savings.

NPS Exit & Withdrawal Rules 2025 — Summary Table

| Scenario | Wealth Threshold | Lump Sum / Periodic Withdrawal | Annuity Requirement |

|---|---|---|---|

| Govt. Retirement | Rs.8 lakh or less | 100% | 0% |

| Govt. Retirement | Between Rs.8 lakh and Rs.12 lakh | Up to Rs.6 lakh | Balance via annuity or systematic withdrawals |

| Govt. Retirement | More than Rs.12 lakh | 60% | 40% |

| Non-Govt. Normal Exit (Age 60) | Rs.8 lakh or less | 100% | 0% |

| Non-Govt. Normal Exit (Age 60) | Between Rs.8 lakh and Rs.12 lakh | Up to Rs.6 lakh | Balance via annuity or systematic withdrawals |

| Non-Govt. Normal Exit (Age 60) | More than Rs.12 lakh | Up to 80% | At least 20% |

| Non-Govt. Premature Exit (Before age 60) | Rs.5 lakh or less | 100% | 0% |

| Non-Govt. Premature Exit (Before age 60) | More than Rs.5 lakh | Up to 20% | At least 80% |

| Govt. Resignation / Removal | Rs.5 lakh or less | 100% | 0% |

| Govt. Resignation / Removal | More than Rs.5 lakh | Up to 20% | At least 80% |

| NPS-Lite / Swavalamban (Age 60) | Rs.2 lakh or less | 100% | 0% |

| NPS-Lite / Swavalamban (Age 60) | More than Rs.2 lakh | Up to 60% | At least 40% |

Conclusion

The 2025 amendments make NPS more humane and flexible. Small subscribers are no longer forced into meaningless annuities. Late joiners are treated fairly. Special situations are handled with more sensitivity.

However, NPS remains a product with strict exit controls, illiquidity, regulatory dependence, and mandatory annuitisation. These rules may change again in the future.

Therefore, NPS should be seen as a supplementary retirement product, not the foundation of retirement planning. For disciplined investors, it can be useful. For those who value flexibility and control, it remains restrictive.